UK insurers revisit pricing as FCA reforms bite back

Tue, 13th Jan 2026.webp)

Four years after the Financial Conduct Authority (FCA) introduced General Insurance Pricing Practises (GIPP), UK insurers are recalibrating their pricing strategies and product designs. Recent market data indicates that the price gap between new business and renewal premiums is beginning to widen once more.

Sarah Vaughan, Director at Angelica Solutions, said the rule changes altered how insurers compete and how they present cover to customers. She linked the changes to higher consumer costs and increased product complexity.

"While the rules have improved pricing transparency, they've also contributed to rising costs for consumers, reduced product comparability, and a growing complexity in how cover is structured and sold", said Sarah Vaughan, Director, Angelica Solutions.

Premium dynamics

One focus for insurers and regulators has been the relationship between prices offered to new customers and those paid by renewing customers. The FCA's intervention targeted price walking, a practice where insurers offered lower premiums to attract new business and then increased prices at renewal for customers who stayed.

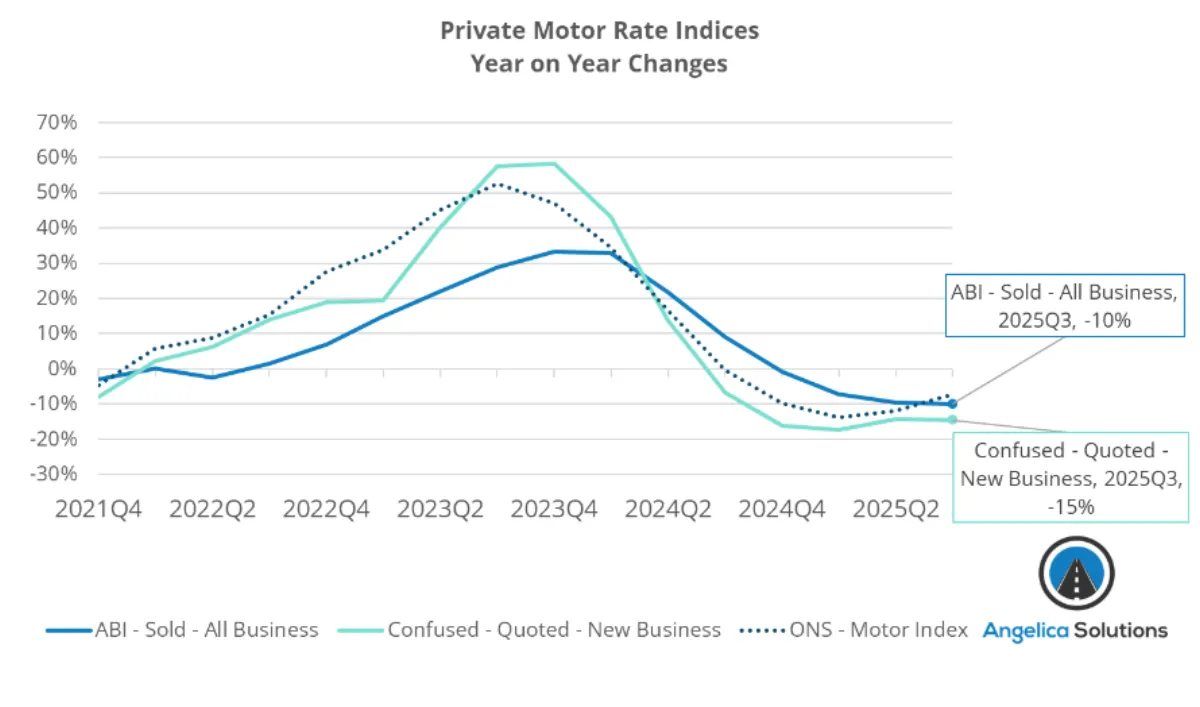

Vaughan pointed to motor insurance as an area where the market is shifting again. She cited EY's 2024 analysis of Association of British Insurers data, which indicated that ratios between new business and renewal premiums in motor are edging back toward levels seen before the reforms.

"While some insurers have adjusted within the spirit of the regulation, others appear to be reintroducing legacy pricing behaviours through different mechanisms. The growing use of tiered or stripped-back products is a prime example, allowing price variation to persist under the guise of choice" comments Sarah, said Vaughan.

Angelica Solutions also highlighted a gap between quoted prices and the premiums customers actually pay. Vaughan cited figures indicating that new business quotes fell by 15% over 12 months to Q3 2025, while average sold premiums fell by 10% over the same period.

Angelica Solutions argued that, if those movements reflect the way new and renewing customers experience the market, renewal prices may have fallen by around 7%. Vaughan said that would weaken the fairness objectives associated with the FCA's approach.

Product structure

Insurers and intermediaries have increased the use of tiered products in personal lines, particularly in motor and home. These structures typically offer a base level of cover with optional add-ons, or a range of product variants with different limits and exclusions.

Vaughan said the spread of stripped-back versions had consequences for how easily consumers can compare policies. She also linked the trend to a higher risk of underinsurance for some customers.

"What we're seeing is a textbook example of regulatory overcorrection," comments Sarah. "Insurers have adapted understandably to protect profitability, but the net result is a market that's more complex and arguably less fair to consumers than before."

Market pressures

Vaughan also flagged pressure on managing general agents in personal lines. MGAs often design insurance products and handle underwriting and distribution, while relying on insurers and other capacity providers for balance sheet risk.

She said regulatory demands and economic conditions are influencing where capacity providers deploy capital. Vaughan said more capacity is moving toward commercial lines. She said that shift reduces innovation and competition in personal lines and pushes premiums up.

Transparency debate

Discussion around insurance pricing transparency has widened beyond the FCA's rules on pricing practices. Vaughan said other consumer finance markets offer more forward-looking pricing information than general insurance.

"There is also a concern that the industry is lacking clear long-term pricing transparency. Unlike sectors such as mortgages or energy, where consumers are offered forward looking pricing or fixed rates, insurance remains opaque.

"As GIPP matures, a thorough review of its macro impacts on pricing behaviour as well as improved product simplicity and differentiation and enhanced clarity on premium progression for both new and renewing customers is needed.

"The Irish market's approach curbing price walking from year one but leaving new business rates open to competitive dynamics could provide useful insight for any review of the GIPP regulation.

"The insurance industry has an opportunity to lead the way in creating a pricing ecosystem that balances transparency, competition, and consumer trust. As we move forward, we must shift the focus from regulatory compliance alone to meaningful reforms that ensure sustainable and equitable pricing for all policyholders"

The Financial Conduct Authority (FCA) maintains a continuous review of general insurance pricing and product governance as part of its broader consumer protection mandate, notably through the Consumer Duty framework. Consequently, insurers are consistently refining their pricing models and product propositions in response to evolving market conditions.