UK card spending falls as missed payments stay high

Mon, 23rd Mar 2026

FICO reported a fall in UK credit card spending in January 2026, while missed payments remained elevated, pointing to continued pressure on household finances at the start of the year.

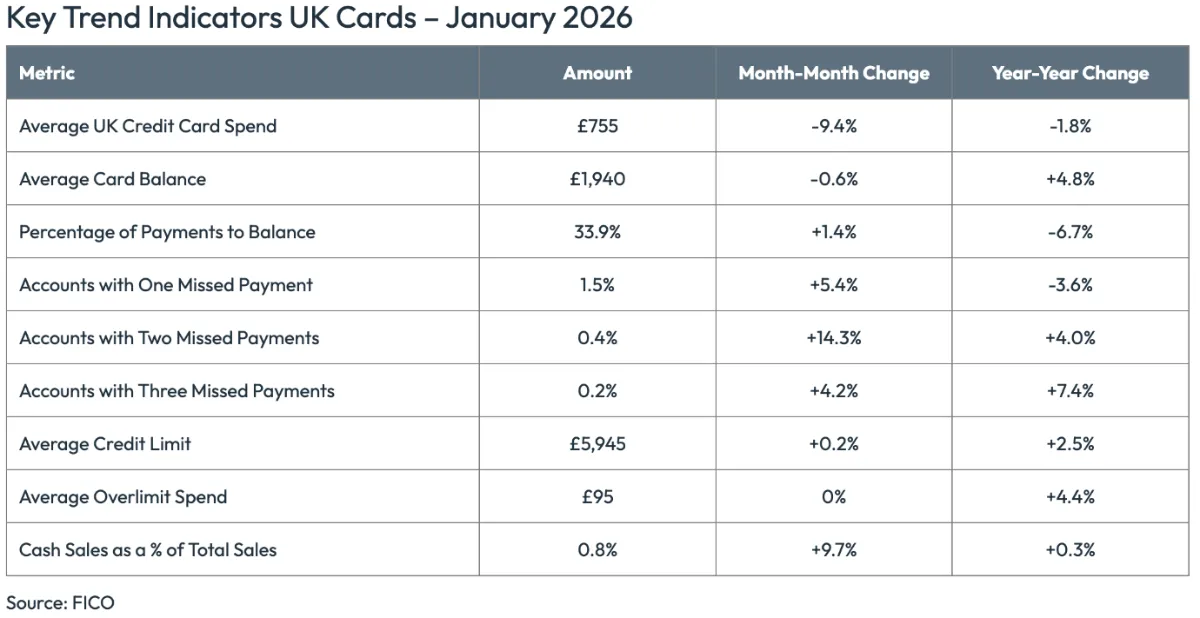

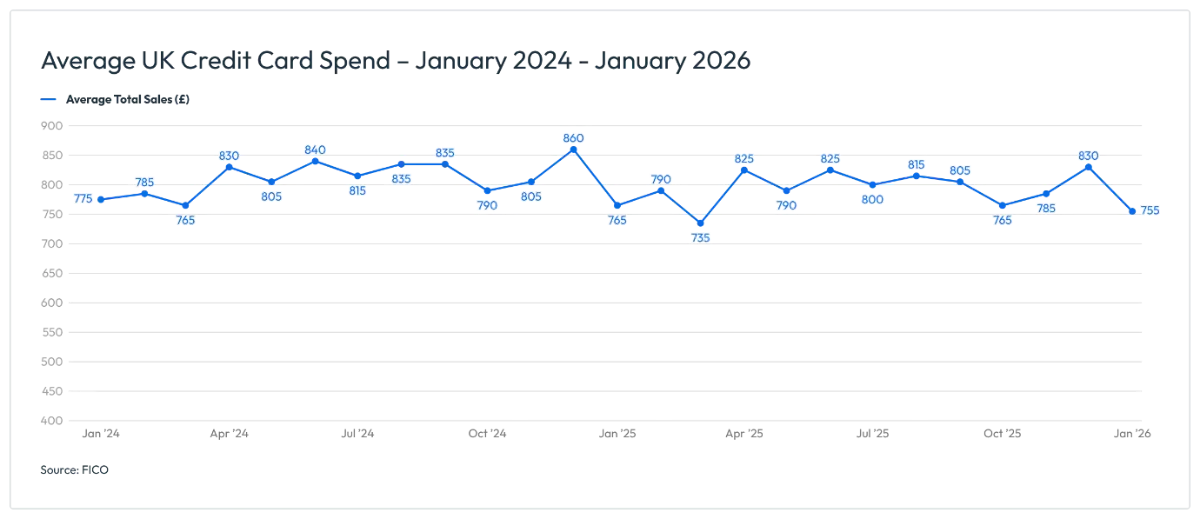

Average credit card spending fell 9.4% from the previous month to £755 in January. That was 1.8% lower than in January 2025, suggesting cardholders cut back after Christmas and spent less than a year earlier.

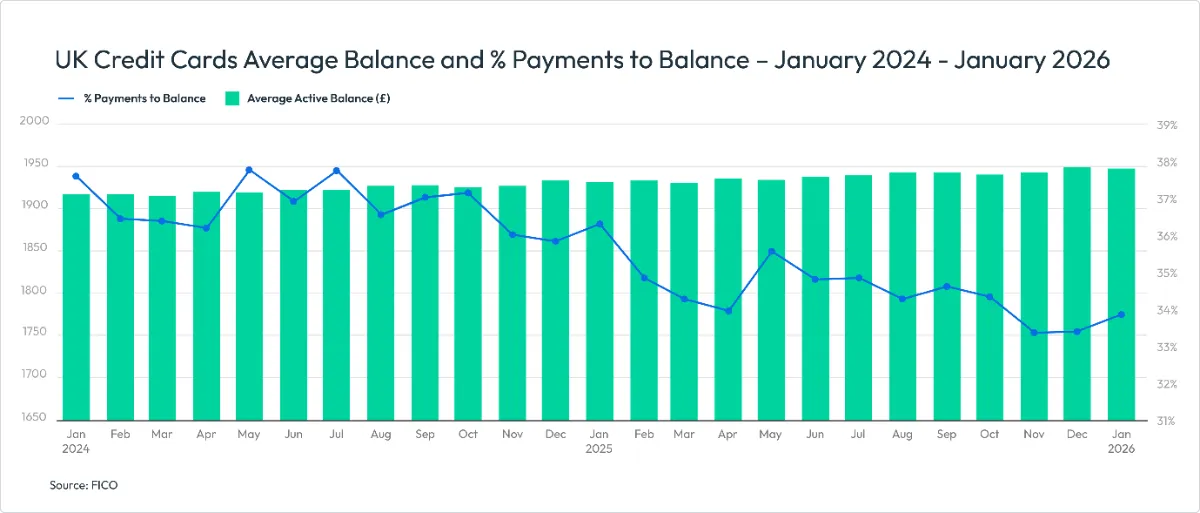

Balances declined only slightly after hitting a record high in December 2025. Average balances fell 0.6% month on month, but remained 4.8% higher than a year earlier.

Repayments improved from December, in line with a normal seasonal pattern, but stayed weaker than last year. Cardholders paid 33.9% of overall balances in January, up 1.4% on the month but 6.7% below the level in January 2025.

The data also pointed to further strain among borrowers already behind on payments. The number of customers missing one, two and three payments all rose from the previous month, while average balances on those accounts were higher than a year earlier.

Accounts above their credit limit increased 6% month on month and 6.2% year on year, a measure often watched as an indicator of mounting pressure on borrowers with little room left on their cards.

Payment strain

One figure stood out in the monthly data: the number of accounts with two missed payments rose 14.3% from December. That points to a worsening position for some households, as customers with repeated missed payments are generally at greater risk of falling deeper into arrears.

The pattern combined lower spending with weaker repayment performance than a year ago, suggesting customers were trying to rein in new purchases while still struggling to reduce existing debt.

These trends follow a year in which higher living costs and borrowing expenses weighed on many consumers. Although January usually brings a pullback after festive spending, the year-on-year comparison suggests the pressures seen through much of 2025 had not eased materially as 2026 began.

The figures are drawn from data shared with subscribers to FICO's Benchmark Reporting Service. The sample comes from client reports generated by its TRIAD Customer Manager system, used by about 80% of UK card issuers.

That gives the data a broad view of the market, covering card usage, balances and repayment behaviour. It also means the January results are likely to be closely watched by lenders for signs of stress among borrowers.

For banks and card issuers, the combination of higher balances, lower repayment rates and rising missed payments can affect both credit risk and collections activity. Lenders typically monitor changes in revolving balances and delinquency trends closely after Christmas, when households often reassess budgets and try to pay down debt.

In this case, many borrowers did make payments after seasonal spending, but not enough to reverse the broader rise in balances from a year earlier. A smaller share of outstanding balances was repaid than in January 2025, even though spending was lower.

FICO said risk and collections teams should remain alert as affordability pressures persist, pointing in particular to the rise in accounts with two missed payments as a sign that financial stress may be intensifying among more vulnerable customers.

"As is typical of January, spend and balances reduced, with customers prioritising payments following seasonal spending. The percentage of overall balance paid showed some improvement, as it typically does in the new year. However, as it remains 6.7% lower than the previous year, it appears that consumers may be more financially stretched than last year," FICO said.

"The combination of this decline in payment rates alongside a 4.8% year-on-year increase in average balances demonstrates that the affordability challenges that defined 2025 have persisted into 2026. Risk and collections teams should focus on proactive intervention strategies, particularly given the 14.3% monthly increase in the number of credit card accounts with two missed payments, which suggests potential acceleration of financial stress among vulnerable customer segments," it added.