UK cardholders carry more debt as spending declines

Thu, 12th Mar 2026.webp)

UK credit card holders carried higher balances through 2025 even as spending fell, according to FICO's analysis of card issuer data. The findings point to sustained affordability pressure and weaker repayment behaviour.

Average balances rose year on year in every month, with growth above 4.5% throughout the year. The average balance reached a record £1,950 in December.

Repayment also weakened. Payment rates were lower than the prior year in every month, meaning customers paid down a smaller share of what they owed.

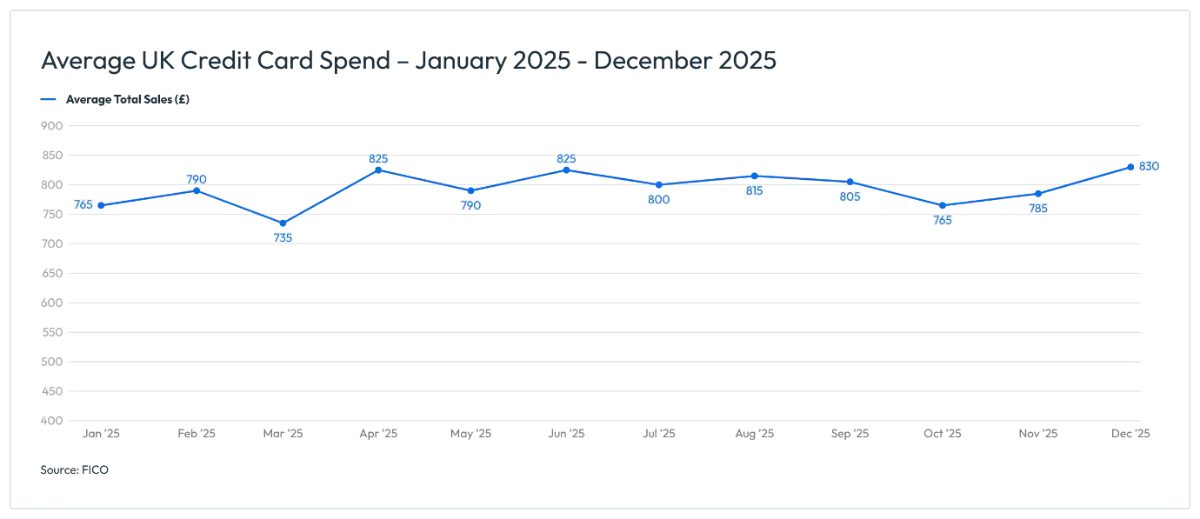

Spending trends

Spending fell versus 2024 from March onwards as cost-of-living pressures intensified. Usage still followed typical seasonality, rising in summer and ahead of Christmas, but peak months remained below the previous year.

Monthly spending reached £831 in December and £826 in June, both lower year on year, according to FICO.

The combination of lower spending and higher revolving balances suggests balances were not lifted by new purchases alone. Instead, weaker repayment appears to have played a larger role, with more debt rolling over month to month.

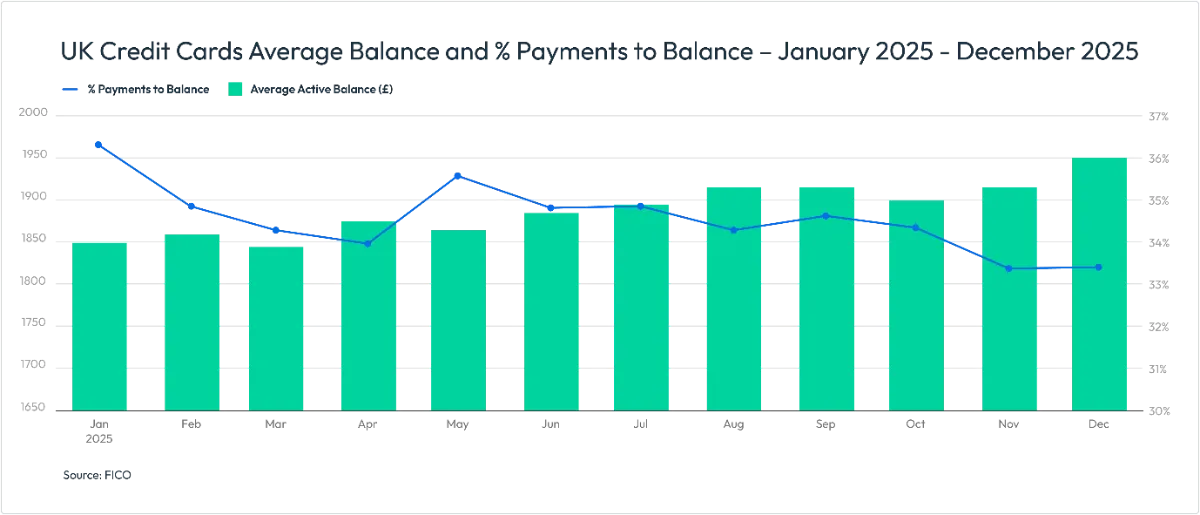

Balances and repayment

Average balances began the year at £1,849 in January, up 4.6% year on year. By December, they were up 4.8% to £1,950, remaining elevated despite reduced spending.

The share of balances repaid fell through the year. The payment rate started at 36.3% in January, down 3.4% year on year, and dropped to 33.4% in November, down 7.4%. It stayed at 33.4% in December, down 6.8%.

Overall, cardholders repaid roughly a third of their balances each month in the latter part of the year. The lower repayment share suggests greater reliance on carrying debt forward even as spending stayed subdued.

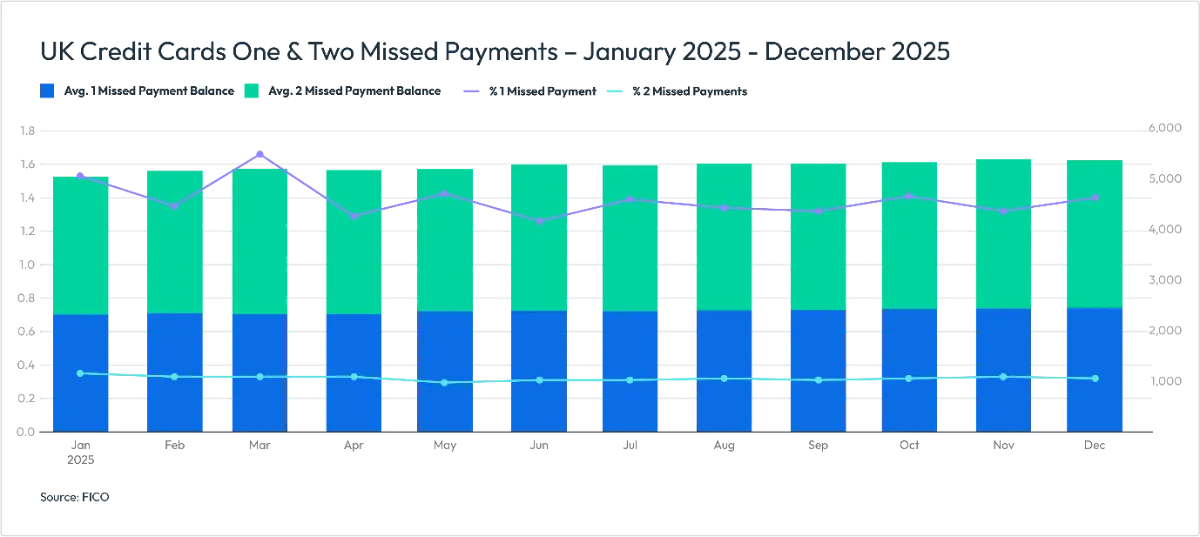

Early delinquency

Missed payments showed a mixed picture. Fewer customers missed one payment than in 2024. However, FICO reported that those who did miss a payment tended to have higher balances, and that balance growth for this group accelerated from May.

Average balances for accounts with one missed payment reached £2,440 in December, an 8.2% year-on-year increase.

More severe arrears moved the other way. The share of customers missing two payments rose from June, while the share missing three payments increased from May. Both measures continued to climb for the rest of the year.

Balances for accounts with two missed payments peaked at £2,938 in November, up 4.9% year on year. For accounts with three missed payments, the average balance rose to £3,324 in December, up 4.1%.

Overall, the data suggests fewer people entered early delinquency, but those who did were carrying larger debts. The rising share of customers missing two or three payments from mid-year also points to mounting stress among those already struggling.

Cash withdrawals

Credit card cash withdrawals followed seasonal patterns, peaking in summer and dipping in winter. FICO said the number of customers making cash withdrawals remained below 2024 levels despite weaker repayment trends.

In the UK, lenders often monitor credit card cash withdrawals as a potential indicator of short-term liquidity pressure. The year-on-year decline suggests this behaviour did not increase overall, even as balances climbed.

Data coverage

The figures come from the FICO Benchmark Reporting Service, based on client reports generated by the FICO TRIAD Customer Manager platform. FICO said about 80% of UK card issuers use the platform, providing broad market coverage.

Outlook for 2026

FICO said other economic indicators still point to continued financial pressure at the start of 2026. It said lenders should focus on earlier intervention as customers approach credit limits, including close monitoring of authorisation approvals.

"Heading into 2026, with other economic indicators still illustrating financial pressures, pre-delinquency intervention strategies will be critical for lenders, with authorisation transaction approvals closely monitored as customers reach their limit. Flexible payment options, affordability reviews, and balance management tools such as spending alerts and caps will help to prevent customers from accumulating high balances in early-stage delinquency."